Health Insurance for Small Business Owners

Are you looking for low-Cost Health Insurance Customized for Small Businesses? Do you have questions on contribution levels, participation rates, and coverage options? In this guide, you’ll find everything you need to know to get started with Small Business Health Insurance, including:

- How to customize benefits

- How to compare options

- Requirements around contribution rates, tax benefits, and participation rates,

- Rules around employees status – full time, 1099’s, seasonal, ect.

Ready to start? Most small business owners do not have the time to research this on their own. As an Independent Agent, I can shop around for the best options for you and your employees.

The Basics – Small Employer Health Insurance Guide

The Texas Department of Insurance is a great place to start to learn the basics. https://www.tdi.texas.gov/pubs/consumer/cb040.html

- What is a small employer? Texas insurance law defines a small employer as a business with two to 50 employers, regardless of how many hours they work.

- What employees do you have to offer health insurance? If you provide health insurance, you must offer it to all your employees who work 30 hours or more each week. You must also offer coverage for their dependents. Business owners can enroll in their small-employer health plan if at least one of their employees also enrolls. Â

- What are the enrollment periods? There is an initial enrollment period (when you first begin our plan OR renew an existing plan). New employees have 31 days from start date to enroll in the plan.  Existing employees that have a life change may have a special enrollment period. If your existing employees do not enroll during the open enrollment period, they must wait until the next year’s open enrollment.

-  Are there waiting periods for new employees? That is up to the employer. You can elect to have no waiting period or select a waiting period. Â

- Note, what you do for one employee, you must do for all.

- How are premiums paid? Most carriers require the employer to pay at least 50% of the lowest qualified medical plan offered for employees only. The remainder of the premium is deducted from the employee’s paycheck. There is one invoice paid per month for all the employees. Â

- Note, there are ancillary benefits (Dental, Vision, Life, Disability) that may be offered as a voluntary benefit. Employees elect which benefit they want and have those premiums deducted from their paycheck.

- What are employers allowed to write off? Consult your tax professional, but in general employers can write off 100% of what they contribute towards their employees benefits.

How to shop for Small Employer Group Insurance

I have created the following model for guiding Small Business Owners on finding the best Group Health Insurance.

Step 1 – Survey your Employees: Ask the basic question – “If we offered Health Insurance as a benefit, who would be interested?â€

- Participation Rates – Many of your employees will be excited to have employer provided coverage. Â

- Their Options will be to enroll as Employee Only (EE), Employee and Spouse Coverage (ES), Employee and Children (EC), or Employee and Family (EF)

- Note, most employers will contribute to the Employee Only (EE) portion, the employee would pay the remainder from their paycheck

- Some may indicate they are covered on their Spouse or Parents (Under 26) plan

- Some may indicate they are have qualified coverage on the ACA Marketplace

- Finally, some may indicate they will not take money from their paychecks to participate in health insurance

- Benefit and Coverage Needed

- Some, based on cost, will want a Low Cost/High Deductible Plan. These plans cover preventative services for free and the remainder of services are subject to deductible. Once the deductible is met, the remainder of costs are covered by the carrier

- Some will want a decent, affordable plan (Basic Option). You select a reasonable deductible and coinsurance plan. Â

- Some want the best plan (Buy Up Plan). These are Gold or Platinum Plans that have a higher deductible but very low out of pocket costs

- Note, based on the size of the group, Carriers allow multiple plans to be offered to employees.

- Step 2 – Have an Agent Shop your options: HERE IS WHERE YOU NEED HELP

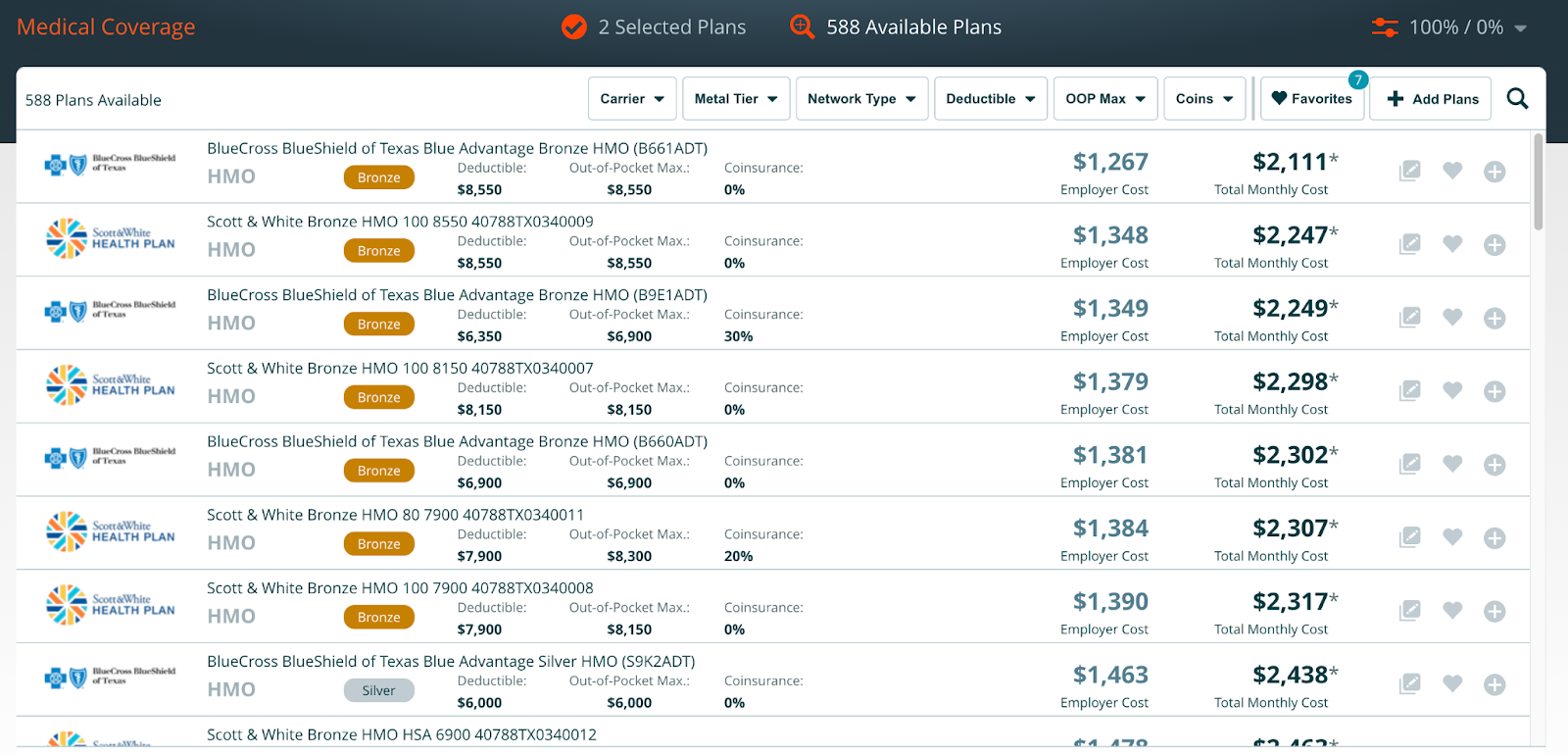

- Here is an example of a small construction company’s options. There are 588 Available Plan options for this company. They will need to wiggle this down based on the following:

- Carrier – If you are in a large market, all the major carriers will have plans. Note, you must pick one carrier for all of your employees. As stated above, you can have different plan options for that carrier

- Metal Tier – Put another way, what deductible and coinsurance do you want to pay? Bronze plans have lower premiums and higher out of pocket / Gold and Platinum plans have higher premiums and lower out of pocket

- Network – Do you want a HMO (require PCP referrals and have no out of network benefits) or a PPO (no PCP referral and out of network benefits)

- Deductible/Out of Pocket Max/Coinsurance – Select a target coverage level to determine costs

- Pretty easy to see why this can get overwhelming, especially since business owners would need to go to each carrier’s website to learn their options. As an Independent agent, I can find you the best options in minutes!

- Step 3 – Determine Fully Insured or Level Funded:  If you have more than 5 Enrolled Employees, you have an option of medically underwritten Level Funded Plan. Here is difference:

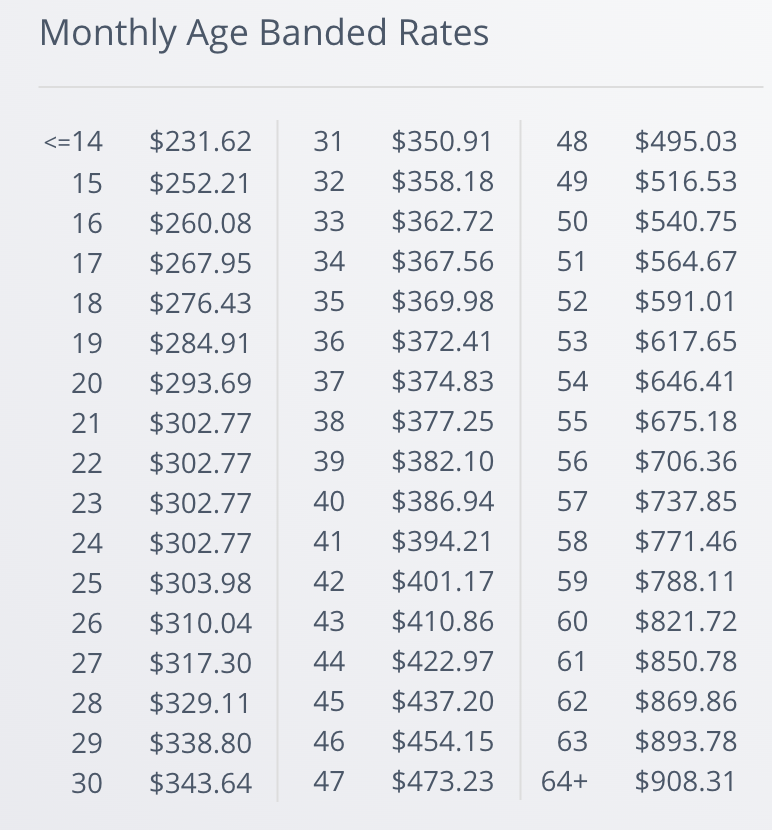

- Full Insured Plans – These are not medically underwritten plans. The costs are based on Age Banded Rates (Below)

- The cost of the insurance is the average age of your employees, based on the coverage options selected.

- This is the only option if you have less than 5 employees enrolling.Â

- This is set it and forget it coverage. The premiums are based on the average risk of all members for the carrier in the age range. Note, the averages include all members including the sick ones.Â

- Level Funded – If you have more than 5 employees that will enroll, Level Funded may be a better option.

- Employees are sent a set of basic medical questions and a list of prescriptions they take.

- The carrier will create your risk model based on the health of your employees.

- If your employees are relatively healthy, the costs of the coverage will lower by up to 30 to 50%. Note, if your employees are deemed risky you will be quoted as Fully Insured Rates.

- The other benefit is you can get money back if your employees remain healthy. At the end or your renewal period, if your total claims amount is less than the amount of premiums, you get money back.  The amount ranges from 50% to 100% of the excess payments. The excess is used as a retention tool to go towards your next year’s premiums.

- On the other end of the spectrum, there is stop loss insurance included in the plan in the event claim volume exceeds premium volume.

- Step 4 – Determine your contribution level and impact on participation rates – It goes without saying that the more you contribute to your employees benefit, the more likely they are to participate. Most carriers will have a participation level requirement. Underwriting will require your past quarter’s State Wage and Tax report to validate the participation rate. Â

- Some carriers require 75% of those WITHOUT existing Qualified Coverage

- Some carriers require 50% of all qualified employees regardless of existing coverage exclusion

- Step 5 – Anticipated Fix the the Family Glitch – Let’s take a look at the family glitch

- Employees whose contribution for self-only coverage is less than 9.83% of household income is deemed to have an affordable offer, which means that the employee and his or her family members are ineligible for financial assistance on the Marketplace, even if the cost of adding dependents to the employer-sponsored plan would far exceed 9.83% of the family’s income. This definition of “affordable†employer coverage has come to be known as the “family glitch.â€Â Learn more – https://www.kff.org/health-reform/issue-brief/the-aca-family-glitch-and-affordability-of-employer-coverage/

- We are still waiting to see what the actual fix will be going into Annual Enrollment for 2023 coverage. The hope is employees will have 3 options:

- Employee and Family do not qualify for tax subsidies (above 600% of Federal Poverty Level) – They will remain on group insurance as is

- Employee and Family qualify for tax subsidies; however, employee’s group insurance is paid 100% or they do not want to change. Employee will remain on group insurance and family moves to ACA

- Employee and Family qualify for significant tax subsidies. Both Employee and Family move to ACA

What happens if your employees say “I need health Insurance, but I can not afford itâ€. Or “I am healthy so I do not need health insurance.â€

I work with many small employers (under 50 full time employees) that have tried to offer group insurance in the past. They struggle to get beyond the first step. Their employees indicate they will not participate either due to cost or other coverage. Another issue is some employers have 1099’s vs. W2’s. It can be difficult to find carriers that will cover 1099’s.  For either situation, there are non-traditional plans that an employer can set up.

- Fixed Indemnity Plans compliment existing coverage. They pay a set amount of out of pocket costs for participants.

- Great for healthy employees that do not find value in group coverage or ACA coverage. They never leverage benefits enough to pay through deductibles.

- Plans cover basic services (up to $6,000 per year) and major medical. Cover injuries, preventative, and illnesses. I always suggest a supplemental accident policy as well.

- The cost of these plans are lower than traditional health insurance. Often, what an employer would pay (50% per employee) for a basic high deductible qualified health plan, will pay 100% for the fixed indemnity plan. Talk to your tax advisor, but contributions towards employees health insurance may be written off at 100% of contribution level.

- Based on the number of employees enrolling, these plans can be a guarantee issue (no medical questions) if written as a group plan.

Want more information on Group Health Insurance?

- Visit https://mccdelivers.com/group-insurance/Â for more information on Group Insurance.

- Schedule time with me to discuss and review your options – https://calendly.com/mccdelivers/schedule-consultation