Need Affordable Health Insurance. Maybe you need Healthy Insurance!

I want to introduce you to Adam and Amy. They are both 38, self employed, and healthy. They currently have a qualified health insurance plan on the Affordable Care Act Marketplace. Like many on the Marketplace, they are extremely frustrated with how much they pay in premiums and out of pocket based on their current deductible. Quoting Adam, “ What’s the point of having health insurance that does not cover anything!â€. Let’s dig into Adam and Amy’s key issue – They have “I have Health Issues Insurance†when they really need “I am Healthy Insuranceâ€. Understanding this difference will save them around $10,000 per year. Their question is “How do I reduce the cost of my health insurance?â€

What is a Qualified Health Plan?

Let’s take a step back to remember why Obamacare was put into law. It ensured people with pre-existing conditions could get coverage and defined Essential Health Benefits. Those are conditions that a Qualified Health Plan must cover. So, if you are in the “I have Health Issues†camp, these changes were significant. If you were not covered by an employer plan, you could get health insurance. It also ensured annual Wellness visits were covered.

- The 80/20 Rule with Qualified Health Plans: There is little debate that healthcare is expensive. Those managing chronic diseases require treatments or prescription drugs to manage those conditions. Health Insurance Carriers are required to pay for all claims and are not allowed to drop members based on claim usage. The reality becomes that a minority of members account for the majority of the claim costs. Those costs need to be spread over the entire covered population.

How does that impact “I am Healthy Insurance�

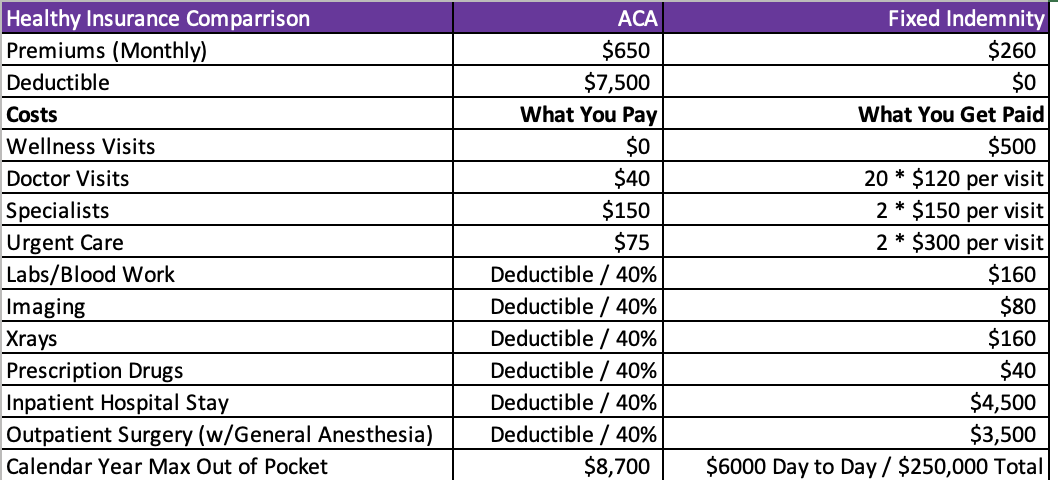

The short answer is deductibles and coinsurance. In a Qualified Health Plan, services beyond doctor visits and wellness visits are subject to deductibles or Coinsurance. You assume the first $5 to $7K prior to the carrier paying a significant portion. The benefit is you will hit a cap (typically around $8,700) where you no longer pay for that year’s claims. This is the augita for Adam and Amy! Based on the fact they are healthy, there is little change of them getting through their deductible. Beyond the basic wellness visits, they can expect to pay for most services. When they do the math, the $650 per month in premiums PLUS the $7,500 deductible, means they need to budget $15,300 a year for health insurance. Thinking about a plan that has a lower deductible? The premiums increase so they would still be in the same boat. Since they rarely go to the doctor, they question the value in having Health Insurance.

Who negotiates your costs : If you are on a qualified health plan, the answer is the carrier. Providers in the network agree to accept the carrier’s usual and customary rate for services provided. These rates are for all providers in the network. Your ability to negotiate is limited or non-existent. This is important when you are paying deductible plus coinsurance. This is why there is focus at the national level for transparent costs in health insurance and no surprise billing in health insurance.

What are Usual and Customary Charges?

Beyond the cost of their insurance, Adam and Amy struggle with Usual and Customary charges. Carriers on the Marketplace have HMO or EPO plans. These plans do not cover out of network providers. Not only do they pay 100% out of pocket for these plans, providers out of network often charge higher costs than what carriers consider usual and customary.

Have you tried to calculate Deductible and Coinsurance?

One of the most frustrating parts of health insurance is the explanation of benefits (EOB). This is sent from your carrier post the provider submitting your claim. It is designed to outline the total cost of the service, what the carrier paid and what you owe. I am currently on my wife’s group plan (note, I will be switching to a fixed indemnity plan!) with a $600 deductible and a 20% coinsurance. I went to my PCP for an office visit, the only time all year I have used plan benefits. The came back as follows:

- Visit Cost – $90

- Carrier portion – $32

- My out of pocket – $58

Note, I worked for United Healthcare/Optum for 8 years. I saw nearly every part of the Healthcare system. Logic would state that I owe $90. You pay the deductible first and then 20% coinsurance until you hit a max of pocket. Totally confused, I called the carrier to see why they paid the $32, the customer service representative could not provide a clear answer. How do I understand my explanation of benefits?

What is the better option for Adam and Amy?

A fixed indemnity health insurance plan. These plans are designed specifically for “I am Health†people. Imagine if a carrier set the claim process and premiums based on fact there is only a small chance you will have major medical bills. Well imagine no further, here it is. For 40% less in monthly premiums, Adam and Amy can get fixed indemnity benefits that will pay them for up to $6,000 in day to day claims. It also has prescription drug benefit and up to $250,000 for calendar year catastrophic (Hospital, Surgery, Emergency Room, Rehabilitation) coverage. The disclosure is they are healthy, these plans do not cover pre-existing conditions for the first 12 months and require basic medical questions answered.

Why this is the best option for Adam and Amy : Based on their health and current usage, they should not experience out of pocket beyond their monthly premiums. Note, I always encourage a supplementary Accident Coverage to provide extra coverage for accidents. That would cost Adam and Amy an additional $32 per month. The final decision was up to Adam and Amy; however, they were comfortable with the Indemnity and Accident Insurance. For $290 per month, they have the coverage they feel the need AND the protection in case of the unexpected. They were eligible as they could pass the basic medical questions. Remember, this is “I need I am Healthy Insuranceâ€.

Lastly, what about Specified Disease Coverage?

We now have Adam and Amy covered for illness, injury and accidents. Almost all of their risks are covered, minus one. What if they are diagnosed with a terminal disease or need an organ replacement? This is referred to as Specified Diseases. My advice is to first check with their current Life Insurance Policy. Living Benefits are riders, within most Life Insurance policies, that allow you to leverage part of the Death Benefit due to a terminal, chronic or critical illness while you are still alive. If you do not want to leverage your Life Insurance Benefit, there are Specified Disease policies available. Adam and Amy could get $225,000 of coverage for $82 per month.

Ready to take control of your healthcare costs?

I will be happy to review these plans and answer all of your questions. Schedule a time at www.mccdelivers.com or give MCC Insurance a call at 210 848 9304.